10 Tips for Saving a Home Deposit

Trying to get into the property market in Australia is not always easy, let alone trying to save 20% to get into the market without having to pay Lenders Mortgage Insurance (LMI). Thankfully we are here to provide 10 tips for saving for a home deposit, along with the current government incentives in place, first home buyers can enter the market with a deposit of 5%, no LMI and stamp duty concessions. Read more about the First Home Buyer Assistance schemes here. So, how does one save for a deposit to enter the property market? In short, discipline, sacrifice, and some good luck!

1. Loan Support Options

Do you have a relative or friend who may be able to assist you with the loan amount? If you are comfortable able to pay back that debt, a loan or a gift from your inner circle is often the quickest way to get into the market.

2. Joint Venture

To minimise the initial outlay of capital on your end see if you can purchase with a partner or friend. This does come with certain downfalls, so the legal arrangements will need to be sorted ahead of time. This will make saving for a home deposit at least a two person opportunity.

3. Work Out The Exact Deposit Amount

Once you have assessed if you can gain assistance from friends and/or family or not, you will need to work out the exact amount of the property you are looking to purchase, then work out the deposit amount.

4. Do Not Waste Money

You will need to establish what is needed vs what is wanted in your everyday life. Change your spending habits to purchase only what is needed. A helpful way to do this is to develop a budget. Having a percentage of your income going to saving for a home deposit.

5. Sell The Items You Don’t Need

Consider selling items that are no longer used, the items sitting in your garage, cupboards and shelves. Not only will this clear you’re clutter but can add significant dollars towards your deposit.

6. Set Up A Forced Savings Routine

Put a certain percentage of your wage into your savings account each payday, before you spend any money. Make this an automatic transfer to save time. Continue this practice forever, and make smart financial habits to get that home deposit.

7. Rent Out Spare Bedroom/s

Now, this step is if your dwelling allows, consider renting out the spare bedroom. This may encroach on your privacy but paying half of your living expenses will add more to your savings than any other savings habit.

8. Consider Eating Out Less

There are monumental savings if you stop the takeout and Uber eats. Instead, opt for cooking at home to save money. As a quick exercise, take a look at your past month of spending on eating out – did the amount surprise you?

9. Consider More Income Generating Activities

If the amount seems too large based on your current income, look at ways you can generate more income such as a second job or starting a side hustle. This is where you turn your passion for something into a business. You may also have share investments in which pay dividends – this is classified as income that can go towards your deposit.

10. Consider Tapping Into Your Super

If your superannuation account has sufficient funds to keep you safe under all circumstances. You could look to use your super to purchase a property if you have a Self-Managed Super Fund (SMSF) set up. This not only works to get your home deposit, but to also works as an investment.

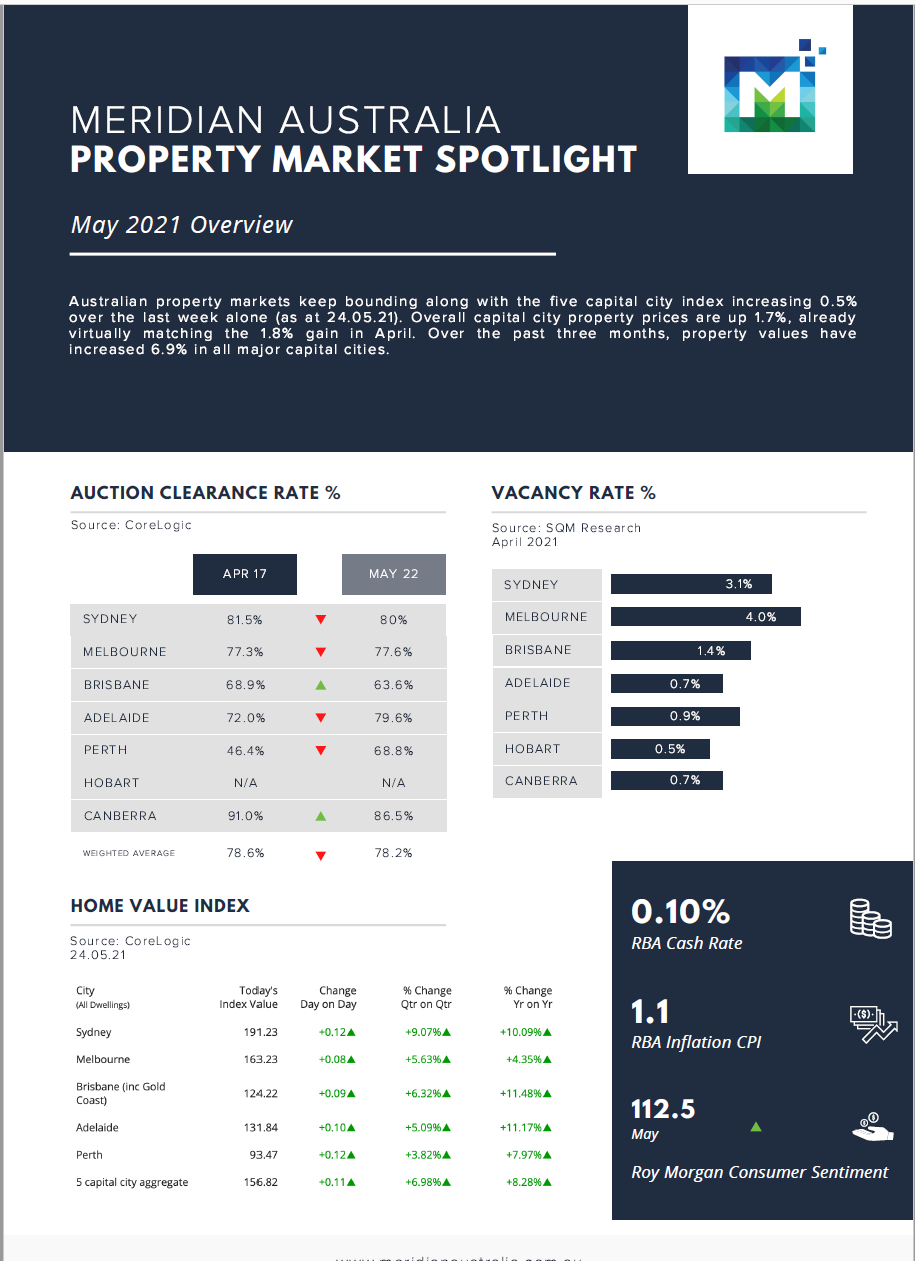

Download the May Property Spotlight Report here

Source: Warren Jacobs – Business Development Manager at Meridian Australia.

For more financial guidance, book an appointment with Financially Sorted today.

For more property investment tips, check out more articles by us.

General Advice Warning

The material on this page and on this website has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained on this page and on this website is General Advice and does not take into account any person’s particular investment objectives, financial situation and particular needs.

Before making an investment decision based on this advice you should consider, with or without the assistance of a securities adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances. In addition, the examples provided on this page and on this website are for illustrative purposes only.

Although every effort has been made to verify the accuracy of the information contained on this page and on this website, Financially Sorted, its officers, representatives, employees, and agents disclaim all liability [except for any liability which by law cannot be excluded), for any error, inaccuracy in, or omission from the information contained in this website or any loss or damage suffered by any person directly or indirectly through relying on this information.